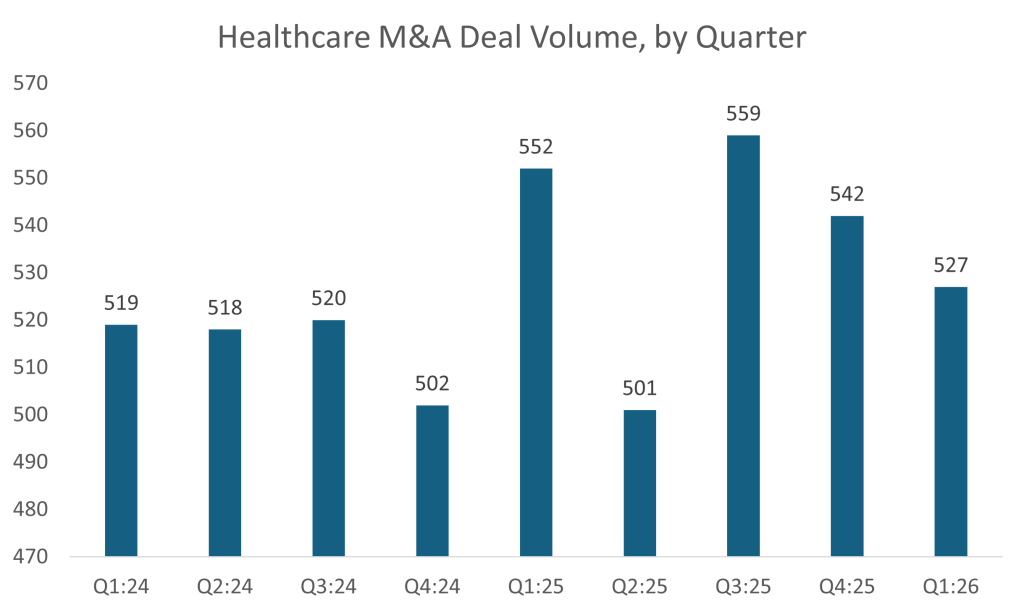

According to data captured in our LevinPro HC platform, healthcare M&A stalled in the first quarter of 2026, reaching only 527 deals, a modest 3% dip compared with the fourth quarter. The difference in volume is small enough to feel almost arbitrary, but these slight quarter-over-quarter variations have become the norm over the past 24 months. As you can see in the chart below, deal volume has remained remarkably stable, aside from outliers in Q1:25 and Q3:25, each with deal activity exceeding 550 transactions.

The steady deal volume suggests that the headwinds and tailwinds from 2024 and 2025 continue to steer the market. We suspect one reason deal volume has remained so steady is the delay in implementing the Medicaid cuts from the “One Big Beautiful Bill” signed by President Trump in the summer of 2025. Those changes are set to begin in 2027, so the market still has time to plan and react, especially in the Hospital and Behavioral Health Care sectors, the two areas that will feel the impact the most.

The Physician Medical Group sector remained the top sector for investors, with 135 deals in the first quarter. As long as reimbursement tailwinds in specialties such as dental and eye care remain strong, we suspect private equity firms and other investors will be pushing heavily into this sector for years to come. Other markets, such as Home Health & Hospice and eHealth, saw an uptick in deal activity, while deal activity in the Hospital market declined, falling to 14 deals, the slowest quarter for the sector in more than a year.

Announced spending, on the other hand, declined significantly. Spending in Q1:26 hit $61.6 billion, compared with $120.2 billion in Q4:25. The last quarter of 2025 was extremely top-heavy, with nearly 20 deals breaking $1 billion in value, but only 11 reached those numbers in Q1:25. The largest deal of the quarter was Boston Scientific Corp.’s $14.5 billion acquisition of Penumbra, Inc., a medical device company that develops products for complex cardiovascular neurovascular conditions.

On the healthcare services side, the largest deal was the $1.1 billion sale of EyeSouth Partners’ retina business to Retina Consultants of America (RCA), a physician management services organization (MSO) formed by Webster Equity Partners in 2020. Headquartered in Southlake, Texas, RCA has more than 215 physicians across more than 300 locations in 20 states. It was bought by Cencora in 2024 for $4.6 billion.

When the deal is finalized, EyeSouth will remain the MSO for its network of non-retinal ophthalmology and optometry practices, including all clinics and surgery centers, which totals about 300 in 20 states.

The press release noted that this deal builds on Cencora’s mission to expand past drug distribution by adding high-margin health services to its portfolio, a trend we’ve been tracking in our database. Just last year, the company also bought OneOncology, Inc. for $5 billion.

These investments in the physician market help Cencora achieve vertical integration with its prescription drug product line, enabling it to capture profit at both the wholesale and provider levels. And the company is not alone in this endeavor; Cencora’s competitors, McKesson and Cardinal Health, have spent billions acquiring large physician networks over the past five years.

Private equity activity increased modestly in the first quarter by 8% to 174 deals, bolstered by a jump in investments in life sciences companies (12 deals) and digital health firms (23 deals), alongside typical favorites such as Physician Medical Groups (66 deals). However, the largest transaction was actually for a home health company, Enhabit, Inc., which was purchased by Kinderhook Industries in a $1.1 billion deal.

Enhabit is a leading national home health and hospice provider with headquarters in Dallas, Texas. The company has a footprint spanning 249 home health locations and 117 hospice locations across 34 states. According to its most recent annual filing, it generated $1.06 billion in revenue in 2025.

Health systems were incredibly active in the first quarter, announcing 44 deals, only 12 of them within the Hospital sector itself. The largest was actually Universal Health Services’ (UHS) $835 million acquisition of Talkspace, one of the best-known telebehavioral healthcare companies. The deal is one of the largest investments by a health system in telehealth and will help UHS expand its reach in outpatient and talk therapy.

Talkspace has a network of about 6,000 professionals offering virtual therapy, psychiatry and medication management. Patients can connect with their clinicians via video, audio, chat or asynchronous text messaging. It serves both employers and health plans.

UHS already has a significant presence in inpatient behavioral health, with nearly 350 facilities nationwide, but Talkspace will help supplement that revenue stream and bring more patients into its ecosystem. While other health systems are focusing on building their outpatient networks through brick-and-mortar locations, UHS is taking a different approach by leaning into telehealth and digital health instead.