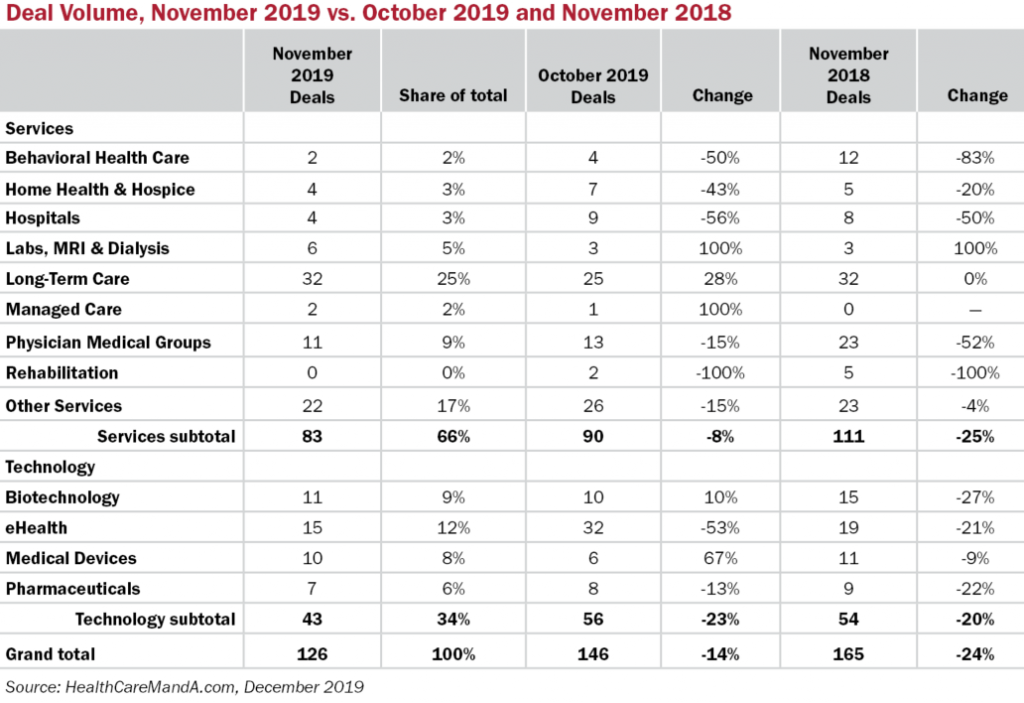

Thanksgiving came very late in November this year, landing on the 28th. That cuts the December shopping season down to four weeks, but it extended the time frame for getting deals done. With a preliminary total of 126 transactions for the month, it doesn’t feel as if anyone was in a rush to close their transactions.

November’s deal volume was 14% lower than the previous month, which now totals 146 transactions. Compared with the roaring 165 deals announced in November 2018, the monthly total is down by 24%. Yes, more deals will pop up on the radar, as they were last month. We started with a total of 136 then and discovered 10 more. That’s how it goes, but 10 more deals here won’t move the needle to the “plus” side.

The year-over-year losses were felt across the board, with all but two sectors showing declines in deal volume. Among the services sectors, deal volume dropped 25%. The Managed Care sector managed to pull out two deals in November 2019, compared with none in 2018.

And the Rehabilitation sector turned in a goose egg (turkey egg?) for November 2019, versus five deals the year before. This sector is getting the cold shoulder from some investors, almost all private equity, who are no doubt waiting to see how the effects of Patient-Driven Groupings Model (PDGM) will play out post-January 1. The rule eliminates the use of therapy service thresholds and changes home health payment from a 60-day episode of care to a 30-day episode.

We know things are slow when every one of the technology sectors posts a year-over-year loss. The four sectors collectively posted a 20% drop, year over year. The usual powerhouse sectors, Biotechnology and Pharmaceuticals, have slowed considerably this year. The Medical Device sector managed to post the smallest decline, only 9%, year over year, as efforts build in Congress to permanently repeal the excise tax that was introduced in 2013 via the Affordable Care Act. The eHealth sector, which had a banner month in October (32 deals), came back to earth with just 15, representing a 21% decline versus a year ago.

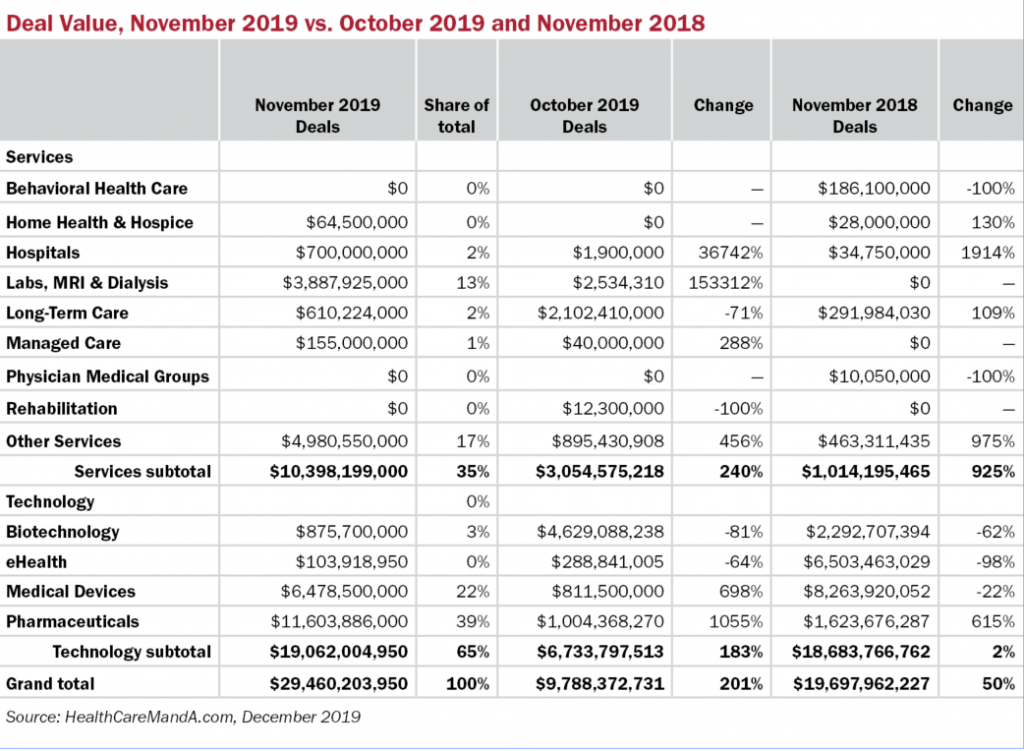

Spending was very strong this month, at nearly $29.5 billion, based on six deals that disclosed prices of $1 billion or more. That puts November 2019 spending 50% higher than last year’s $19.7 billion and about 200% higher than the previous month’s $9.8 billion.

The biggest deal, at $9.7 billion, was announced late in the month by Novartis (NYSE: NVS), targeting The Medicines Company (NASDAQ: MDCO) and its promising cholesterol-reducing drug candidate inclisiran. Medical device giant Stryker Corporation (NYSE: SYK) announced its $5.4 billion takeover of Wright Medical Group N.V. (NASDAQ: WMGI), whose upper and lower extremity products complement Stryker’s business lines, perhaps too closely.

Without those deals, November’s spending would be a more modest $14.4 billion, still higher than October (+47%) but lower than last year (-32%).

December deal volume seems strong, but it’s still early days. We’re not going to see another record-breaking year like we did in 2018, which now stands at 1,901 transactions. That’s OK. Next year will be interesting.