Looking back, the third quarter got off to a great start. The Dow topped 27,000 and the S&P 500 passed 3,000 within the first two weeks. The NASDAQ followed, rising past 8,000 in about three weeks from the start. All were boosted by the Fed’s lowering its interest rate by a quarter point at its July meeting. Another rate drop followed in September, but by then, the markets were recovering from the chaos that hit in August.

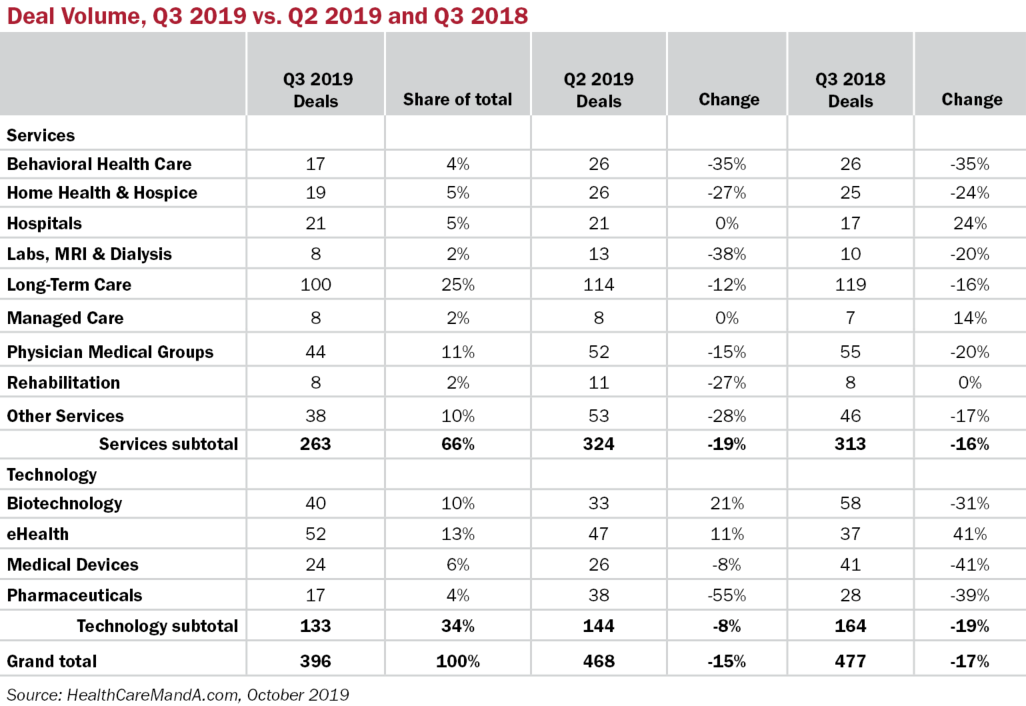

Through it all, healthcare deals held steady. Early results show the third quarter’s deal volume remained strong, with 396 deals now on the books. That preliminary figure is 15% lower than the 468 deals announced in Q2:19 and 17% behind the same quarter in 2018, when we were in the midst of a record year for healthcare deals.

Deal volume didn’t mimic the equity markets and stayed relatively steady across July (136 deals), August (131) and September (130). We expect to turn up a few more transactions as earnings season progresses.

The Long-Term Care sector carried the day with a sixth consecutive quarter of 100-plus deals. Although Q3:19 logged precisely 100 deals, which now looks like a 12% decline compared with the second quarter, that total will bump up in coming weeks as more deals surface. The digital health sector also posted strong gains over last quarter (+11%) and a year ago (+41%). Electronic health records and revenue cycle management companies are perennial best sellers in this sector, but artificial intelligence-driven analytics for a range of sectors—clinical trials, laboratory tests and population health management, for example—are coming to the fore.

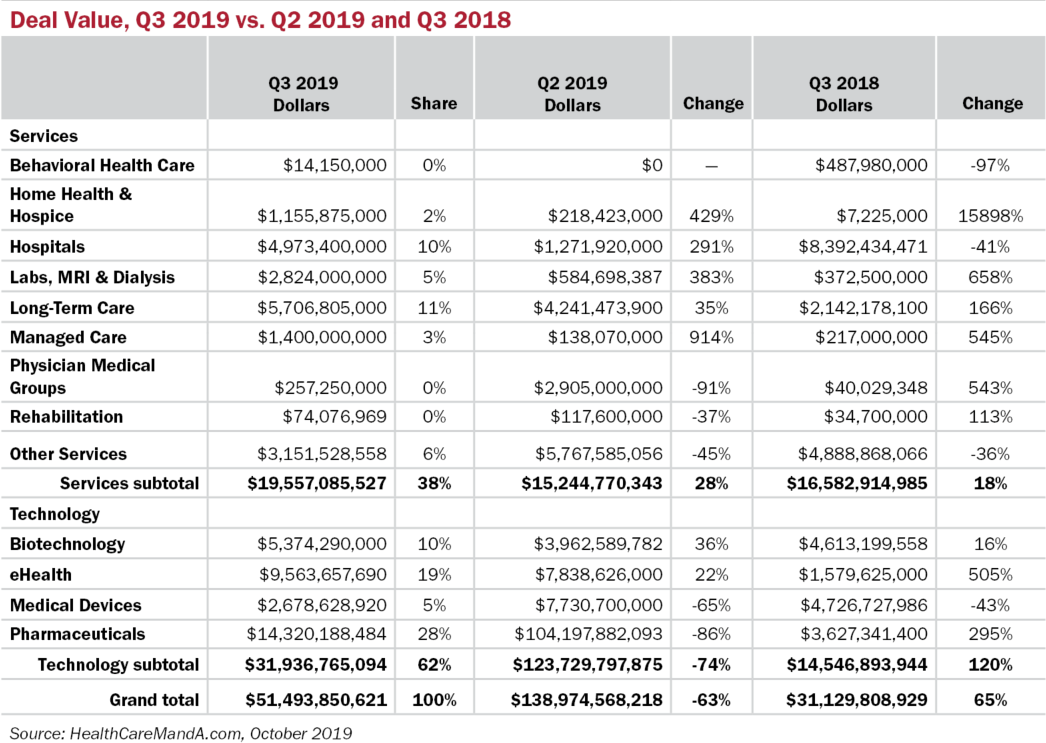

Spending in the quarter, at $51.5 billion, was healthy, as in “normal, not outrageous.” This quarter has a hard comp versus the second quarter, with a 63% drop against Q2’s $139 billion in combined spending. That’s what we mean about an outrageous total—it’s the result of the $87 billion bid for Allergan plc (NYSE: AGN) by AbbVie (NYSE: ABBV) and Pfizer’s (NYSE: PFE) $11.4 billion deal for Array BioPharma (NASDAQ: ARRY). Compared with the same quarter in 2018, with $31.1 billion, spending this year was actually stronger, by 65%.

What’s in store for the rest of the year? Sources tell us that deal flow looks steady through the fourth quarter, though some deals may spill over to the first quarter of 2020. That prediction isn’t as robust as we’ve heard in other years, when the fourth quarter was expected to explode with deals racing to beat the December 31st deadline.

We may still see more action than in the third quarter. Private equity firms have a lot of dry powder stored and are poised to use it, if the right target comes on the market. In the third quarter, Hospice Compassus, a 25-state hospice services company owned by Audax Private Equity and Formation Capital, went to a joint venture between TowerBrook Capital Partners and not-for-profit Ascension, the largest Catholic health system in the world with facilities in 23 states. We’ve heard the target had “north of $60 million in EBITDA” and went for more than $1 billion.

A major behavioral health care platform just came to market. BayMark Health Services, a portfolio company of Webster Capital, is the largest opioid treatment company in North America with 218 programs across 32 states and one Canadian province. The company has announced 15 acquisitions since its launch in 2016, the most recent being its purchase of Recovery Services of New Mexico in April 2019 for an undisclosed price. There’s a lot of buzz around BayMark, so we could be seeing another busy quarter on the services side, at least.