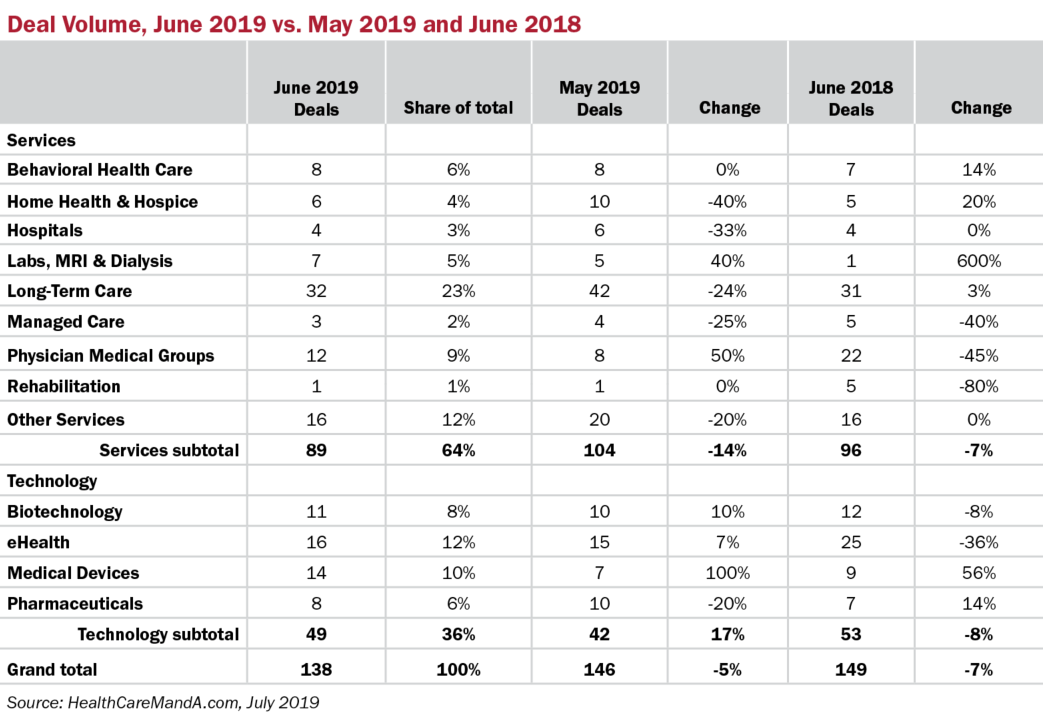

Healthcare mergers and acquisitions turned in another strong performance in June, on the heels of a busy month in May. Preliminary data shows 138 transactions announced, just 5% below the previous month’s 146 and 7% behind the same month in 2018.

The Long-Term Care sector led the way, as usual, with a 23% share of the month’s total deal volume. With 32 deals reported, deal activity wasn’t as strong as it was in May (42 deals), but stayed on par with the 31 deals announced the year before.

Two sectors posted big gains, year over year. The Laboratories, MRI & Dialysis sector saw a 600% increase, albeit on only seven deals. The Medical Device sector realized a 56% jump over last year’s results and a 100% increase over the previous month.

The Behavioral Health Care and Home Health & Hospice sectors each posted slight gains compared with June 2018, while the Managed Care, Physician Medical Groups and Rehabilitation sectors all underperformed compared with a year ago. The Rehab sector usually posts single-digit deal volume, so a decrease of four deals year-over-year made for an 80% drop in deal volume. At least some of the softening this sector is experiencing is coming from the uncertainty around the Patient-Driven Payment Model scheduled to take effect on January 1, 2020. Although it’s targeted to the home health industry, it could impact physical therapy reimbursement.

Private equity firms made 17 acquisitions in June. Only three announcements disclosed prices, the largest being $2.7 billion. Goldman Sachs’ (NYSE: GS) private equity arm, West Street Capital Partners VII, agreed to pay that amount for Capital Vision Services, dba MyEyeDr. Canadian firm DW Healthcare Partners announced two deals, buying two medical device companies.

Just four hospital transactions made the definitive agreement stage in June. However, three U.S. health systems made acquisitions in June, as Providence St. Joseph added Bluetree, a consulting and strategy company specializing in Epic health solutions; LECOM Heath acquired a 110-bed skilled nursing facility; and Wyoming County (NY) Community Health System acquired two family medical practices.

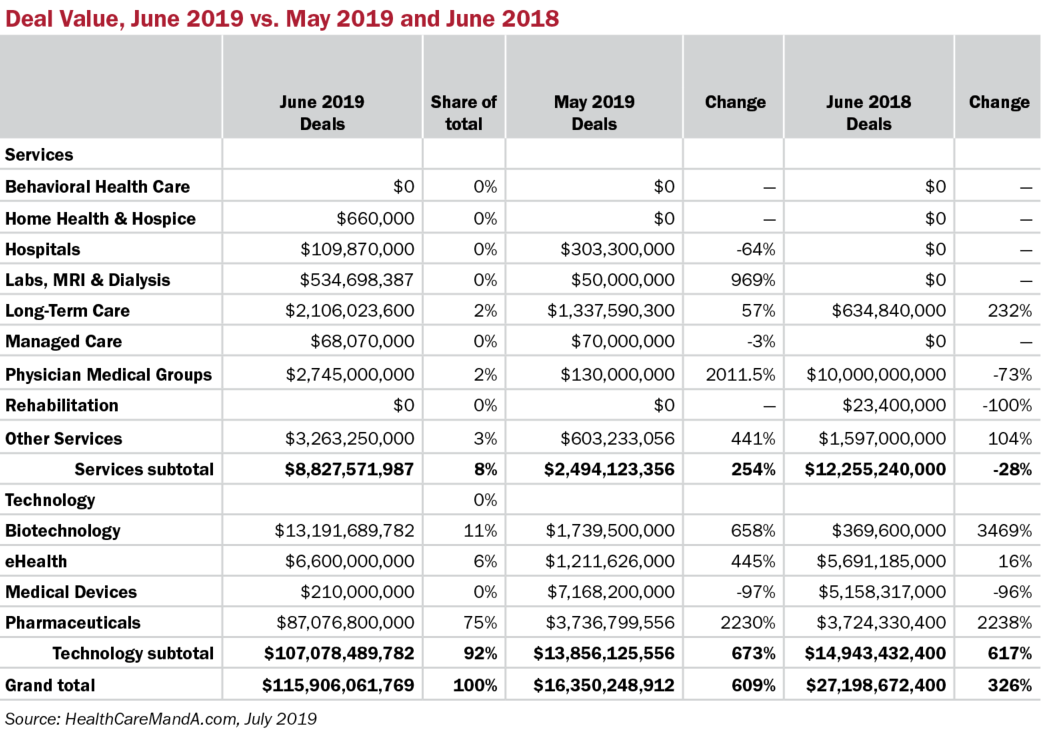

Spending for the month was out-sized, at nearly $116 billion, thanks to the $87 billion Allergan (NYSE: AGN) acquisition announced by AbbVie (NYSE: ABBV). Even without that deal, the month’s spending would have been a healthy $28.9 billion, beating May’s $16.4 billion by 77% and last year’s total of $27.2 billion by 6%.

Biotechnology, eHealth and Pharmaceutical targets accounted for six of June’s top 10 deals, based on price. The second largest deal in June was Pfizer’s (NYSE: PFE) $11.8 billion acquisition of Array BioPharma (NASDAQ: ARRY) , followed by Dassault Systemes’ (Paris: DSY) $5.8 billion deal for Medidata (NASDAQ: MDSO).

Dealmaking in 2019 has followed the typical cycle of slow first quarter, faster second quarter. Third quarter activity is often slower than the second, but we aren’t seeing signs of slowing in the first 10 days of July. Stay tuned.