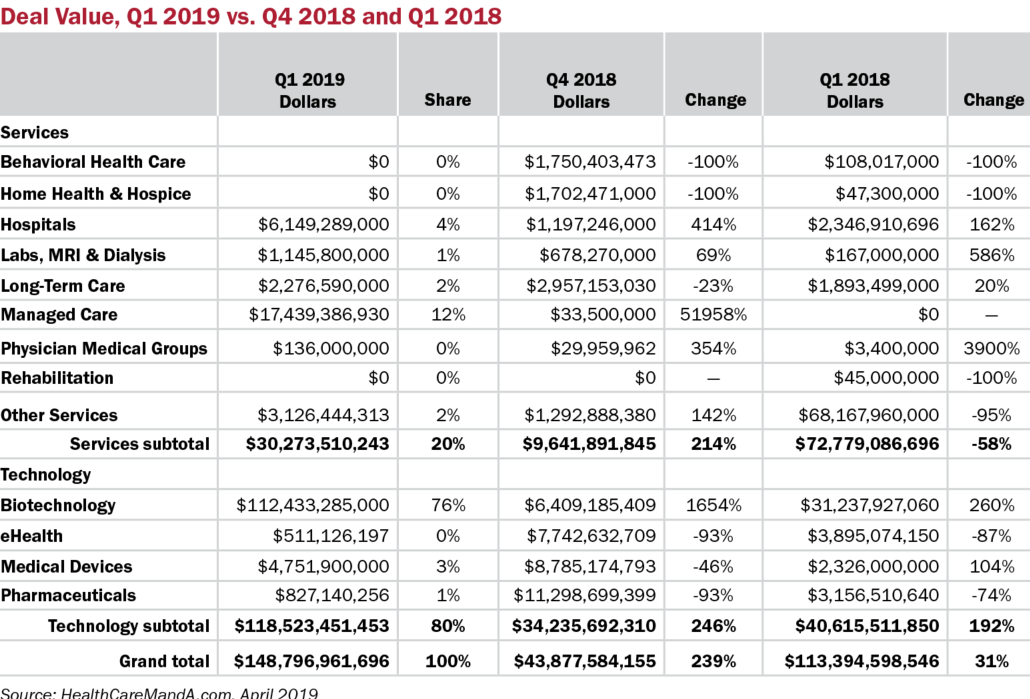

Spending in the first quarter, totaling $149 billion, beat both the previous quarter (up 239%) and the year-ago time period (up 31%). Three deals had a combined total of $113 billion, accounting for 76% of that spending.

Without those three, the first quarter would have ended with approximately $36 billion, which would be 18% lower than the fourth quarter of 2018 ($44 billion) and 68% lower than the first quarter in 2018 ($113 billion).

Those big deals began coming early on, beginning with the $74 billion acquisition of biotech biggie Celgene Corp. (NASDAQ: CELG) by Bristol-Myers Squibb (NYSE: BMY) on January 3. The deal put Bristol-Myers deeper into the highly competitive and highly uncertain oncology market. It could be the biggest deal in all of 2019, but it’s too early to call.

In February, Danaher Corporation (NYSE: DHR) announced its $21.4 billion deal for GE Healthcare’s (NYSE: GE) biopharma business, which provides instruments, consumables and software that support the research, discovery, process development and manufacturing workflows of biopharmaceutical drugs. About a month later, we have the $17.4 billion acquisition of WellCare Health Plans (NYSE: WCG) by Centene Corporation (NYSE: CNC).

All told, there were 11 deals with prices higher than $1.0 billion, six of them in Biotechnology sector—and four of those six targeted oncology treatments of some type. It’s a pattern that will likely play out throughout the next three quarters.

Technology is fueling much of the activity we’re seeing, in the eHealth and Medical Device sectors, naturally, but also in deals for telehealth startups or teleradiology labs announced by companies in the Hospital, Physician Medical Group and Home Health & Hospice areas. That’s a big reason the eHealth sector stayed nearly as busy in Q1:19 as it did in Q4:18. With the job market still flexing its muscles, technology is expected to make up some of the shortfall in health care. Check back in July.