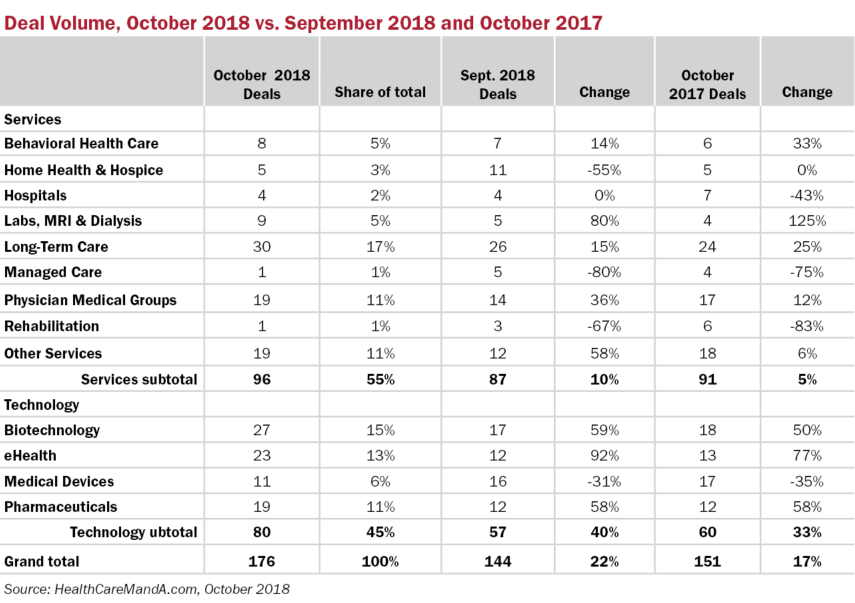

Healthcare transactions kicked into high gear in October, with preliminary data showing a monthly total of 176 deals, the highest monthly tally reported this year. It bests September’s 144 deals by 22%, and the year-ago volume of 151 deals by 17%.

Eight of the 13 sectors saw solid gains compared with October 2017 results. The Long-Term Care sector saw a boost to 30 deals, up 15% compared with the previous month, and 25% year over year. Behavioral Health Care, Physician Medical Groups and Other Services were strong performers among the services sectors, and the usually quiet Laboratories, MRI & Dialysis sector showed a surge (relatively speaking) of 80% compared with the previous month and 125% versus October 2017.

Among the technology sectors, only the Medical Device category under performed compared with those two earlier months, down 31% versus September and down 35% against October 2017. Even as the Trump administration and the CMS are making moves to corral high drug prices, the Biotechnology and Pharmaceutical sectors saw deal volumes top previous months’ totals by 50% or more.

The real star was the eHealth sector, with 23 deals, up 92% over September and 77% year over year. Consolidation among digital health companies was the driving force behind a majority of the deals, while private equity firms only accounted for three transactions.

The breadth of this sector’s targets also attracted buyers from other healthcare sectors, and strategic acquirers looking to add a healthcare component to their wider offerings. In the former category, Medical device maker Varian Medical Systems (NYSE: VAR) acquired Finnish digital health company Noona Healthcare, the financial and credit management firm TransUnion (NYSE: TRU) acquired revenue cycle manager Rubixis, and women’s health company Prima-Temp added Kindara Inc., which developed a successful fertility platform.