Talk about saving the best for last. For months, deal volume has stagnated, slipped, and failed to excite. Then December happened. Six deals with prices over $1 billion were announced, and their combined value was $91.7 billion.

Of course, the CVS/Aetna (NYSE: CVS/AET) deal accunted for most of that, at $77 billion. But what counts is that these deals showed the game is changing in the healthcare market, and market forces and investors are working outside the usual Medicare/Medicaid reimbursement policies.

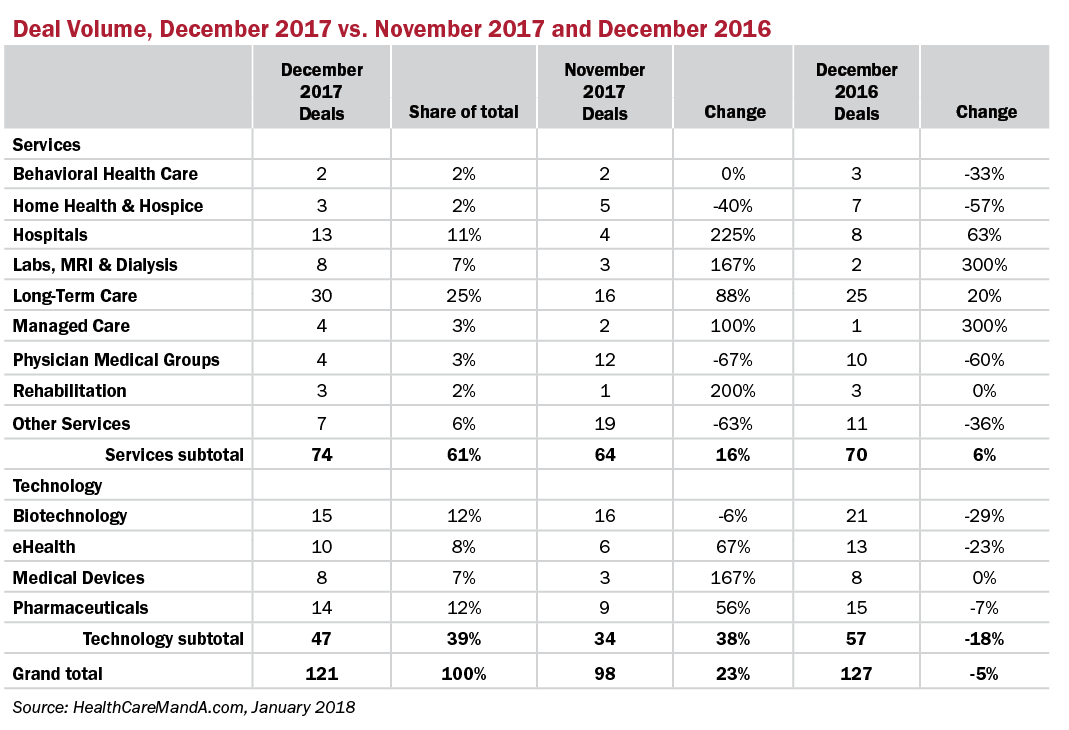

Let’s start with December’s deal volume. At 121 transactions (so far, more will undoubtedly be added), the total is up 23% compared with November’s 98 transactions, but 5% lower than the same month a year ago. We’ve reported far slacker monthly totals almost every month in 2017, so this is news.

Credit where credit is due. The Republican tax legislation passed in late December. The bill gave big business great leeway to U.S.-based corporations to bring overseas cash home without dire tax consequences, as well as lowered the official corporate tax rate to 21%. The law’s passage will have great ramifications for American corporations, not all involved directly in the healthcare market just yet. But our money is on Apple (NASDAQ: AAPL), Google (NASDAQ: GOOG) and others to double down on efforts to break into this space in 2018 and beyond.

Besides the obvious CVS/Aetna game-changer, bringing healthcare to consumers in a retail/pharmacy setting, the country’s largest health insurer, UnitedHealth Group (NYSE: UNH) and its Optum subsidiary made a second aggressive move into the physician medical group space with the $4.9 billion acquisition of DaVita Medical Group (NYSE: DVA). The December deal followed last January’s announcement that it was buying Surgical Care Affiliates (NASDAQ: SCAI) for $3.4 billion.

In the same month, UnitedHealth announced a $2.8 billion deal for Banmedica SA (SSE: SGO), a Chilean healthcare company with hospitals, health plans and much more. Don’t blink, or you’ll miss the growth outside the United States.

This is one month when the Technology sector’s prices couldn’t compete with the Services side. With a total of $94.5 billion for the month, December’s dollar volume is far beyond anything seen in 2017. The Services sectors made up 94% of the combined total in December.

But thanks to Congress’ tax legislation, we safely predict there will be a return to big pharma (as in Big Pharma) deals in 2018. Some have already percolated up to the top, such as Mallinckrodt’s (NYSE: MNK) $1.2 billion acquisition of Sucampo Pharmaceuticals (NASDAQ: SCMP) announced on December 26. The Pharmaceutical sector has declined 53% in deal volume from its record high of 188 deals in 2014. Preliminary data shows just 89 transactions announced in 2017. Oh, the crocodile tears we can’t shed for this sector. Rest assured, 2018 will be a memorable year, if not a record-breaker for global pharma deals.

Here’s to 2018. Stay with us to see how it works out.