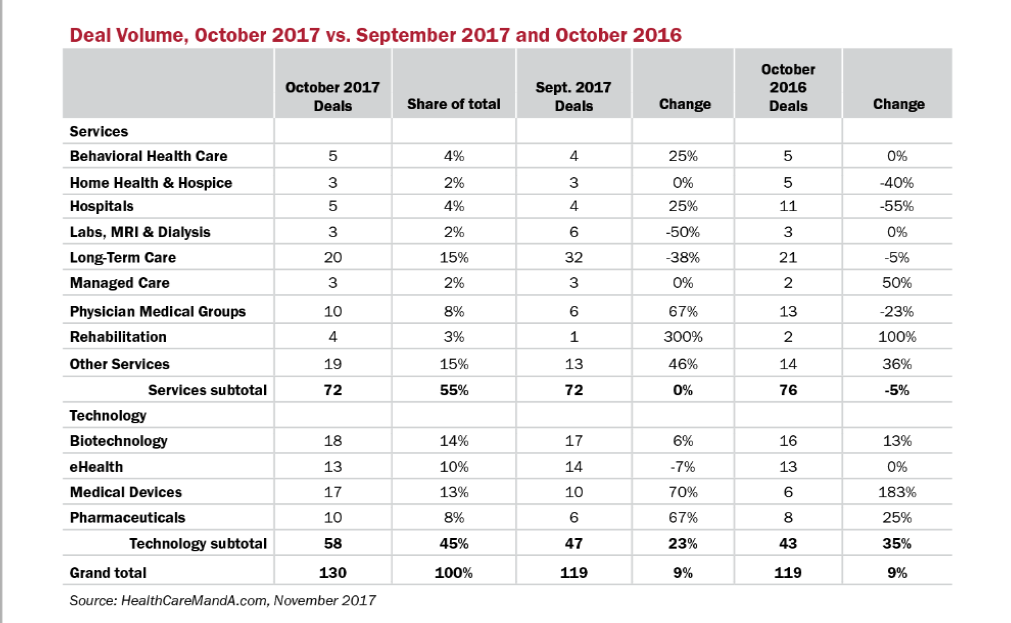

After a few months of slow going, healthcare deal volume revved up in October. Although it’s the start of the typically busy fourth quarter, we’ve learned not to expect past performance to indicate future results. Preliminary data shows 130 transactions were announced, up 9% compared with the 119 deals announced in both September 2017 and October 2016.

Deal value was comparatively strong, as well. The $12.1 billion reported for October 2017 is 4% higher than the previous month ($11.7 billion), but 8% lower than the same month a year ago ($13.2 billion). Three deals came with $1 billion-plus prices and a combined total of $8.5 billion, or 70% of the month’s spending. By contrast, September had two billion-dollar deals totaling $4.8 billion, which made up only 41% of that month’s total.

Deal volume is the best indicator of the healthcare market’s strength, in other words. October marked the end of the services sectors’ strong performance. A year ago, those sectors accounted for 64% of the month’s deal volume, and 61% in September. Their share fell to 55% of October 2017’s volume, which is a more typical level.

Long-Term Care transactions have been on a roller coaster ride in recent months. Early data for October shows only 20 announcements, down 38% compared with the previous month. The decrease was probably inevitable, since September’s 32 transactions represented a 26% jump from August (24 deals). A year earlier, this sector posted 21 transactions, and we’re sure there will be at least one or two closings still to be announced from October 2017 to even up the year-over-year comparison.

The Medical Device sector staged a strong performance in deal volume, posting 17 transactions in October, up 17% over September and 183% compared with October 2016. This sector has turned out a steady stream of deals in 2017, which now total around 98 transactions and nearly $47 billion in spending. With two months left in the year, it’s possible this sector will exceed 2016’s annual total of 113 deals, and perhaps the $61 billion recorded then.

The largest deal of the month, by disclosed prices, was Novartis AG’s (NYSE: NVS) $3.9 billion acquisition of Advanced Accelerator Applications S.A. (NASDAQ: AAAP), a Swiss radiopharmaceutical company developing molecular nuclear medicines. It’s the first company takeover of the year for Novartis, which has announced at least five research collaborations or licensing deals but spent just $262 million on those.

The Pharmaceutical sector has been in a protracted slump in 2017, with none of the mega-billion-dollar takeovers that were so common in 2014 and 2015. That may be about to change in 2018, if the Republicans can get their “tax reform” legislation passed by the end of December. The bill was unveiled on November 1, and will undoubtedly undergo myriad changes before it becomes law. But its corporation-friendly bent will remain intact, we’re betting, and could spur Big Pharma to spend bigly on foreign competitors.

November is only a few days old, but deals are pouring in. It may be a busy fourth quarter, after all.