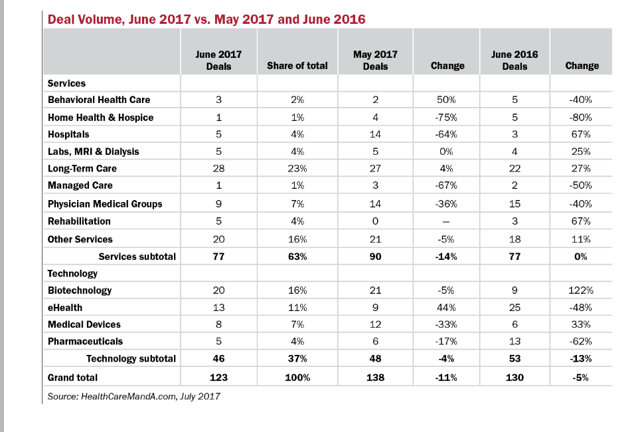

Preliminary data for the month of June shows that investors are still bullish—or at least comfortable—betting on health care. Some 123 transactions were announced last month, an 11% decrease compared with May’s 138 transactions. Year over year, however, this early data is just 5% below the 130 deals announced in June 2016.

For a little perspective, April 2017’s deal volume was just 104 transactions, which made the May numbers look very strong by comparison. June’s deal volume looks reassuringly healthy, as it is close to the year-ago total, and could be adjusted upward in the future as more deals come to light.

The same trends we’ve noted in previous months are still playing out, too. Deal volume in some services sectors—Laboratories, MRI & Dialysis, Long-Term Care. and Other Services—has remained steady, if not strengthened.

The Hospital sector has bounced up and down, transaction-wise, from month to month. Only five deals that were truly a merger or an acquisition reached the definitive agreement stage in June, although several partnerships and affiliations were announced as well. That contrasts sharply with May’s 14 hospital transactions, representing a 64% drop from month to month. May’s deals, however, were largely the result of Community Health Systems (NYSE: CYH) finding buyers to take at least nine hospitals off its books, a crusade that has been ongoing for the past 12 months as the company rationalizes its portfolio yet again. Real estate investment trusts (REITs) have been very active in this sector in 2017, as we’ve noted in previous issues, and we don’t expect that trend to slow down for some time, either.

On the technology side, the Biotechnology and Medical Device sectors are busy consolidating, while eHealth deals continue along their erratic month-to-month path and Pharmaceutical deals are stuck in neutral gear.

Spending on healthcare deals is always erratic, when viewed from month to month. For that reason, it’s not alarming that June’s $17.1 billion total was about half of May’s $32.7 billion total. Six multi-billion deals were announced in May 2017, totaling $27.7 billion, comprising approximately 84% of the whole. By contrast, there were five billion-dollar-plus deals announced in June, but their total was just $12.5 billion. Those deals accounted for 73% of the month’s total.

For what it’s worth, spending in June 2017 was 19% higher than in June 2016 ($14.3 billion). There doesn’t seem to be a significant push to finish big deals by June 30, the end of the month, the second quarter and the first half of the year. If a deal is that big, it’s better to get it right than to rush it to meet a deadline. That said, December 31 is always a different story.

Looking ahead, the Senate Republicans may finally get their healthcare bill on the floor for a vote in the week after the Fourth of July recess. There was still a lot of division in their ranks before the holiday, but constant reports of deal-making have kept speculation high that there will be some movement this month. Either way, investors do not seem overly concerned. Pragmatic is more like it. □