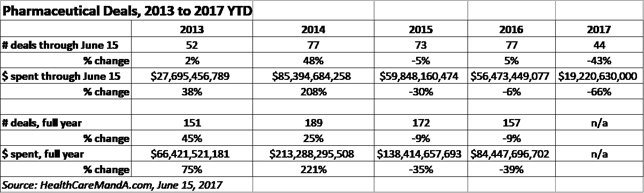

The rising cost of prescription drugs was part of many candidates’ campaign platforms in the 2016 national elections. The topic has not gone away, and is certainly a factor in the dearth of Big Pharma deals in 2017. Through June 15, M&A in the Pharma sector is down 43%, to 44 transactions, compared with the same period in 2016, which had 77 transactions.

Spending is also down in for the first six months of 2017. Through June 15, acquirers announced $19.2 billion in committed financing, down 66% from the same period in 2016, when approximately $56.5 billion was spent.

There are deals being done, regarding this issue, but most are not M&A. In fact, several managed care organizations and drug companies recently announced value-based agreements, following several in 2016.

In May, Optum, the healthcare services business of UnitedHealth Group (NYSE: UNH), and Merck (NYSE: MRK) will collaborate to develop a shared “Learning Laboratory” to explore value-based and pay-for-performance models, known as Outcomes-Based Risk Sharing Agreements (OBRSAs). The project will also look at the potential for broad adoption among health insurance companies, pharmacy benefits managers (PBMs), and pharmaceutical companies.

Realize that Optum’s OptumRx segment is one of the largest PBMs in the country, and that Optum’s integrated claims and clinical records will be used to provide data reflective of real-world patient care and outcomes in the United States. These data assets will enable the companies to assess OBRSA models across different patient populations, clinical settings, and therapeutic areas aligned with Merck’s drug portfolio.

A few days later, Harvard Pilgrim Health Care, a not-for-profit health services company based outside of Boston, signed two outcomes-based contracts with AstraZeneca (NYSE: AZN) for medicines to treat acute coronary disease (Brilinta) and Type 2 diabetes (Bydureon).

In 2016, Eli Lilly & Co. (NYSE: LLY) announced a pay-for-performance agreement with Harvard Pilgrim on the GLP-1 drug Trulicity, under which it traded a formulary upgrade for rebates that depend on patients’ blood sugar targets.

Harvard Pilgrim also announced an outcomes-based deal on Novartis‘ (NYSE: NVS) heart failure drug Entresto, following in the wake of Cigna (NYSE: CI), which announced in May 2016 that it was signing on to Novartis’ pay-for-performance plans for Entresto. Cigna previously announced similar deals for new cholesterol-fighting drugs from Amgen (NASDAQ: AMGN), Sanofi (NYSE: SNY) and Regeneron (NASDAQ: REGN).

Pfizer Spurns Price Limits

Several pharma companies have pledged to limit price hikes on their drugs to single-digit increases, including AbbVie (NYSE: ABBV), Allergan (NYSE: AGN), Novo Nordisk (NYSE: NVO), Sanofi and Takeda (OTC: TKPYY). Rather than pledge to lower prices, Eli Lilly, Merck and Johnson & Johnson (NYSE: JNJ) issued “transparency reports” to show how their rebates and discounts to PBMs were helping to lower drug costs.

Then came Pfizer (NYSE: PFE). On June 1, 2017, hiked U.S. prices of 91 drugs by an average of 20%, including Viagra and Lyrica. The company had also raised prices in January, according to Reuters, and those were included in the average reported in June.

That hasn’t sat well with legislators, and may produce some backlash. On June 13, 2017, the U.S. Senate Health, Education, Labor and Pensions (HELP) Committee held a series of hearings on the growing cost of prescription drugs and how the delivery system in the United States affects patients’ out-of-pocket costs. PBMs were in the spotlight, as were the rising costs of generic drugs long used by patients to keep their prescription costs low.

Finger-pointing by various lobbyist groups aside, the effect on drug prices will likely be minimal. The effect on pharma M&A will be like an ice-cold blanket.