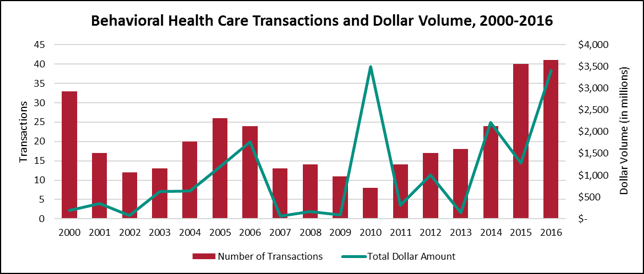

The Behavioral Health Care M&A market has enjoyed six years of strong growth, following passage of the Affordable Care Act in 2010. The market peaked at 41 deals announced in 2016, with $3.4 billion in combined spending.

Despite the uncertainty surrounding the ACA’s replacement, merger and acquisition activity is still strong in the early months of 2017. Tailwinds are stronger than headwinds. Destigmatization of addictions, mental health issues and other disorders has brought attention to the care needed by millions. There is still significant, unmet need in many sub-sectors, such as acute care psychiatric beds. De novo building is easing some of that need, and could lead to more consolidation in a few years.

One of the hottest areas in this sector is addiction and substance abuse treatment programs and facilities. Of the 41 deals announced in 2016, 19 targeted this sub-sector. Eleven transactions targeted mental health programs or inpatient psychiatric facilities; six were for programs dealing with intellectual or developmentally disabled individuals; and four were for educational or counseling programs working with children and families. A single deal was for a gero-psychology program focused on seniors.

Thanks to the ACA’s emphasis on accountable care organizations and population health management, many hospitals and health systems are looking for quality providers to come into their markets and help them address behavioral health challenges in their communities. This is not a core competency for most hospitals, even though an estimated 25% of patients showing up in emergency rooms have some behavioral health diagnosis.

U.S. health systems are looking for affiliations or partnerships, rather than outright acquisitions. Only two hospitals announced acquisitions of behavioral health groups in 2016, and both targets were foreign-based entities. Universal Health Services (NYSE: UHS) acquired UK-based Cambian Adult Services Group from Cambian Group plc, for $479 million. The target had 81 behavioral health facilities with 1,193 beds at the time of the announcement in December.

The second hospital-acquirer was Germany’s MEDIAN, a joint venture between Waterland Private Equity and Medical Properties Trust. The target was AHG Allgemeine Hospitalgesell-schaft AG, one of the largest treatment treatment providers in the fields of psychosomatic medicine, addictions and sociotherapy. It operates 45 hospitals, treatment centers and outpatient clinics with 4,000 beds. Financial terms were not disclosed in this transaction.

Reimbursement becomes more uncertain if the ACA is completely repealed, but most providers know behavioral health care is a necessary part of their population health management efforts.

Valuations Are Still Strong

Valuations in this sector haven’t changed much in recent years. Platforms still command higher valuations than practices do, although some analysts note that sellers who have practices still want the valuations that platforms garner. As one analyst put it, “This market isn’t frothy, like other sectors that are tired or outplayed. It’s fragmented.”

In the addictions/substance abuse segment, some companies are trading at 11x to 12x EBITDA (those would be the platforms), while others are going for 7x to 8x EBITDA.

Inpatient psychiatric hospital operators have the opportunity to grow organically by building and opening facilities in new markets. They don’t have to pay the valuation multiple, in those cases, and attract interest from the major U.S. players, Acadia Healthcare Company (NASDAQ: ACHC) and Universal Health Services. If things get competitive, multiples could reach 10x to 12x.

Also, metrics are now more important, from a clinical perspective, as strategic buyers and private equity investors look to validate the valuations they’re paying. The ability to couple metrics with clinical protocols differentiates an organization from the more traditional local behavioral health provider.

Distinguishing factors that lead to more aggressive multiples include a good EBITDA base, a solid management team, a long acquisition pipeline and the opportunity to build de novo programs and centers. Who wouldn’t want to buy a company like that?

For more insight into this growing sector, check out our recent webinar, “Behavioral Health Care: Buying, Selling & Valuing”.