Uncertainty is the hobgoblin of the merger and acquisition markets, and the month of June was a high point (or low point, depending on your perspective) for anxiety in global financial markets.

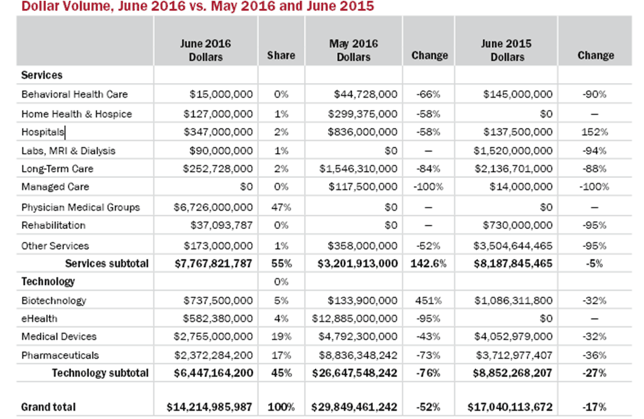

Still, the healthcare deals kept rolling in. Our preliminary total for June 2016 stands at 115 transactions, exactly equal with the same month a year ago. Compared with May’s total of 141 deals, though, June’s total does look as if someone is applying the brakes. It takes 12 months to make a year, though, and one month’s results do not create a trend.

The digital health sector turned in the strongest gain compared with June 2015, when only two deals were announced. This June, 22 deals were announced in the sector, for a 1000% increase. The usual targets such as revenue cycle management and telehealth companies were represented, but more and more targets serve niche markets. For example, RBP Healthcare Technologies provides electronic health records, care coordination and other services through a cloud-based technology platform, but those services are specific to the behavioral health care sector. (Inspira Financial Inc. paid $8.5 million to acquire it.) And iLab Solutions provides cloud-based services focused on core laboratory management to universities, research hospitals and institutions. Agilent Technologies (NYSE: A) did not disclose financial terms on that acquisition.

Spending was not as robust as in year-ago quarter, at $14.2 billion (-17%). The largest deal in June 2016 was the $6.7 billion merger between AmSurg (NASDAQ: AMSG) and Envision Health Holdings (NYSE: EVHC). In June 2015, the largest deal was only $2.1 billion (Allergan [NYSE: AGN] buying Kythera Biopharmaceuticals), but there were six deals priced at $1 billion or higher in that month, for a total of $9.8 billion. By contrast, the largest deal in May 2016 weighed in at nearly $12.9 billion, as Quintiles (NYSE: Q) acquired IMS Health (NYSE: IMS).

Two pharmaceutical companies made multiple sales in June. Teva Pharmaceutical Industries (NYSE: TEVA) made approximately $1.59 billion by selling various portfolios of generic drugs to three willing buyers. Those deals were made to satisfy the FTC’s requirements in the wake of Teva’s 2015 acquisition of Allergan’s (NYSE: AGN) generic drug business for $40.5 billion.

AstraZeneca (NYSE: AZN) continued to divest non-core assets as it licensed the rights to seven anesthesia drugs to Aspen Global Inc. (OTCBB: ASPU) for $520 million, and sold the rights to its gout drug, Zurampic, in Europe and Latin America to Grünenthal GmbH for $230 million.

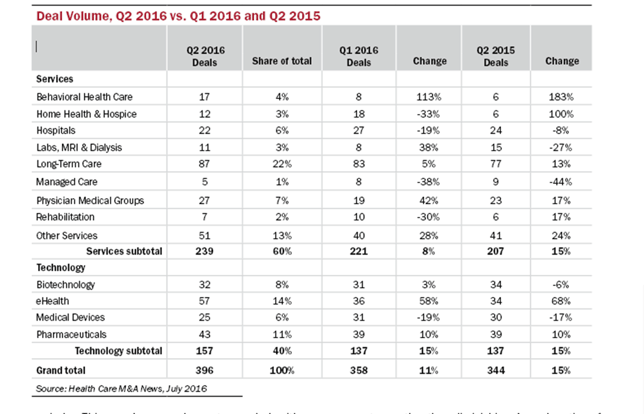

As noted in the story on page 1, healthcare M&A is running slightly ahead of 2015, comparing the first six months of each year. At 754 deals (+5%) and $168.9 billion (+4%) in spending, this year’s results could surpass the records set in 2015 (1,505 deals and $397.0 billion).

Thanks to Brexit’s effect, however temporary, on the global financial markets, it is unlikely the Federal Reserve will raise interest rates in the near future. Talk of another recession is growing, but looking back on the top line data, healthcare M&A didn’t take a hit during the Great Recession. This could be a very good year, indeed. □